A piece written by polling & opinion research consultant, Adrian Macaulay.

Over the years, polling and opinion research has enabled our firm to acquire a better understanding of how Canadians understand and perceive the country’s agriculture and agri-food sector.

Each new wave of research allows us to ask new questions, test hypotheses, explore new policy areas, as well as measure to what extent opinions and attitudes towards the sector have changed over time.

In the process of analyzing the data we collect, we try to examine not only how Canadians overall view a particular topic or issue, but whether one or more demographic sub-groups (ex: men, those 25-34, Atlantic Canadians, etc.) have a more pronounced effect on the overall distribution of attitudes towards an issue.

Alternatively phrased, we try and see to what extent a particular sub-demographic over- or under-performs in relation to the sample overall (in this case: Canadians overall).

Depending on the topic at hand or the way you ask the question, some demographics push more than they pull, some demographics pull more than they push.

In the past few years of measuring opinions towards Canadian agriculture, we’ve noticed that age and region are two demographics that tend to exhibit more pronounced differences between sub-groups when considering how the agri-food sector is seen overall, in relation to other sectors, or on issues that view the sector more holistically.

Fewer differences can be found between men and women, education levels, and income brackets when examining how Canadians view sector-wide issues. However, differences between these demographics do exist and can be found.

Differences in income categories tend to be more evident around financially-focused topics such as our most recent questions about food shopping and consumption habits in the past year, or how large of a barrier different financial obligations are to affording food.

Research conducted this year found some differences between men and women around the topic of food insecurity: women (91%) were more likely than men (77%) to say hunger and food insecurity will be very or somewhat serious problem in the near future.

Education is usually the quietest of the five major demographics we take into account. Few significant differences are found between different education levels with respect to how the sector is viewed overall. Having said that, some of our polling from 2021 found that those with lower levels of education (high school education or less) had lower levels of nutritional literacy than those with higher levels of education.

Regional differences are more commonly found in questions that view the agri-food sector overall such as Canadians’ proximity to agri-food and exposure to agriculture, how optimistic/pessimistic Canadians are of the sector’s growth potential, and perceptions around the costs of food.

It can be argued that [older Canadians] are a critical demographic sub-group for the agri-food sector, in that they provide sector with source of strength.

Like a majority of Canadians from coast to coast, younger age cohorts (<35) are trusting and supportive of agriculture, however, their enthusiasm for farming pales in comparison to those 55+.

Older Canadians are much more likely to hold stronger, more supportive feelings towards the sector than younger Canadians.

Some of the more notable areas where older and younger Canadians part ways around agriculture and agri-food are:

- Agriculture’s influence on the Canadian economy

- Agriculture’s environmental footprint

- Willingness to purchase products “made in Canada”

- Protein consumption

When asked to rate the importance of different sectors on Canada’s economic landscape, those over the age of 55 were more likely than Canadians overall, as well as younger age cohorts, to rate agriculture as a ‘5’ meaning it was of very large importance to Canada’s economic landscape.

While not as clean-cut as the views towards Canada’s economic landscape, we asked a very similar question that used ‘critical infrastructure’ instead of ‘economic landscape’ and found that older age cohorts are more likely to rate agriculture as a ‘5’ or of very large importance to the country’s critical infrastructure.

When we asked Canadians whether they had made any changes to their food shopping and consumption habits (from a list provided), those over the age of 55 were more likely than Canadians overall to say they opted for domestically grown or produced food over food imported from elsewhere.

When asked whether they would be more or less likely to purchase a series of food categories if they were grown or produced in Canada, those over the age of 55 were more likely than Canadians overall to say they would be purchase each of the categories listed if they were domestically produced.

Our polling has also found that older Canadians are more likely than Canadians overall, as well as those under the age of 24, that agricultural practices currently in place today are less harmful for the environment compared to the past.

Taking into account the findings above, one might be able to argue that younger Canadians may prioritize, or take interest in, different issues than older generations. Our research has found generational differences between age cohorts around protein consumption and interest in red meat alternatives.

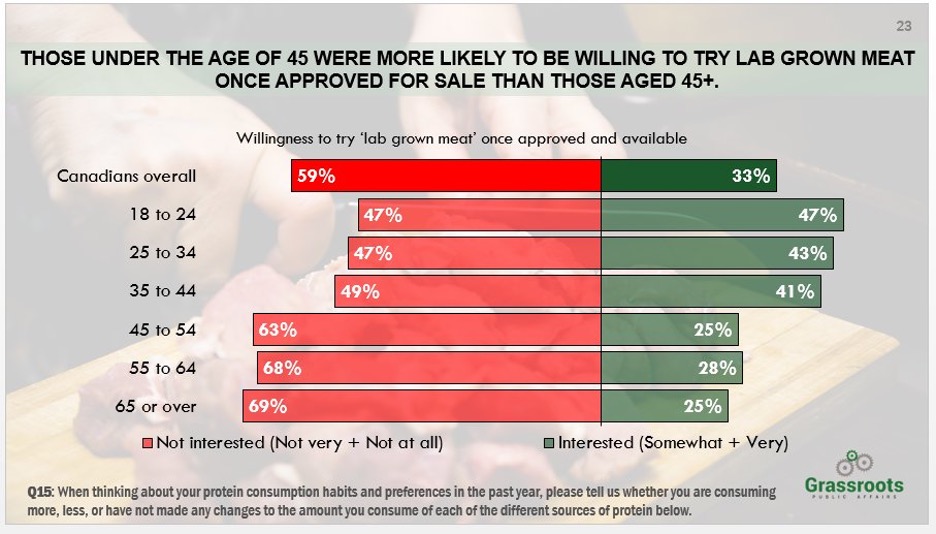

In 2021, Grassroots measured opinions and attitudes towards lab grown meat. Among those who say they had heard of or are aware of the term ‘lab grown meat’, noticeable differences in interest can be found between those above and below the age of 45. Younger Canadians were more interested in trying lab grown meat than older age cohorts, as well as Canadians overall, while those over the age of 45 were more likely to say they were not interested in trying lab grown meat.

Differences between older and younger cohorts go beyond the lab: older Canadians were more likely than Canadians overall to say they were eating more poultry in the past year.

In 2021, we found those between 25-34 were more likely than Canadians overall to say that they had consumed ‘somewhat’ more plant-based protein products in the past year, while those 55+ were more likely than Canadians overall to say that they cannot or do not eat plant-based protein products.

In this year’s wave of research, we found those 18-34 were more likely than Canadians overall to say they were eating more (‘somewhat’ + ‘a lot’) plant-based protein products in the past year.

While it’s good news that Canada’s agri-food sector has a strong and dedicated base of support among older Canadians, that support network may not be sustainable over time and the sector must do what it can to ensure that younger Canadians view the sector positively (especially as they age).

Despite all of the insights and findings we have uncovered over the years, one thing our polling is unable to do at the moment is explain why noticeable differences exist between older and younger age cohorts around the topic of agriculture. Furthermore, we have not fully identified all of the different areas that older and younger cohorts may differ on.

Further research is needed to get a better understanding of the functions and tensions between age cohorts.

While those who work in the agri-food sector are best positioned to ask relevant and important questions that will influence a desired outcome, below are three high-level research topics that might be worthy of consideration:

- From a list [major problems or obstacles] AND [opportunities and advantages] the agri-food sector must work with, which issues resonate most or least among the different age cohorts

- How do the different age cohorts see agriculture as a profession and as a possible career path – either as someone’s first job or for someone transitioning from another field

- Explore and measure the dietary habits and interests of different age cohorts and gauge to what extent the sector can use those habits as a communications plank to build interest or support.

By better understanding the interests and motivations of younger Canadians around agricultural topics, the sector would be able to grow and maintain support more efficiently over time.

Adrian Macaulay

Polling & Opinion Research Consultant

Leave a Reply

Want to join the discussion?Feel free to contribute!